Alberta, Gold, & Bitcoin

Alberta, Gold, & Bitcoin

Alberta's Sovereignty Act without monetary independence is just that; an act

Alberta is a province in Western Canada. It has the third largest proven oil reserves in the world, trailing only Venezuela and Saudi Arabia. It is also a major agricultural exporter. It boasts the highest average income in Canada; the hardworking, independent, and entrepreneurial nature of its populace leads it to lean heavily to the conservative side politically.

Readers who are new to the value propositions of gold and bitcoin, or to the history of money in general would benefit by reading “The Bullish Case for Bitcoin” by Vijay Boyapati, found here

In January and February of 2022 Canada’s internal strife found itself on the world stage. A convoy led by long haul truckers that has come to be known as the “Freedom Convoy” made its way to the nations’ capital of Ottawa to demonstrate. Ostensibly, these protests were a response to Prime Minister Justin Trudeau’s use of vaccine mandates as a wedge issue in a failed attempt to win a majority government (detailed here and in the video link below). Those familiar with Canada and in particular Western Canadians -who instigated the protests and were most heavily represented- know that the considerable animosity on display for those few weeks has much deeper historic origins.

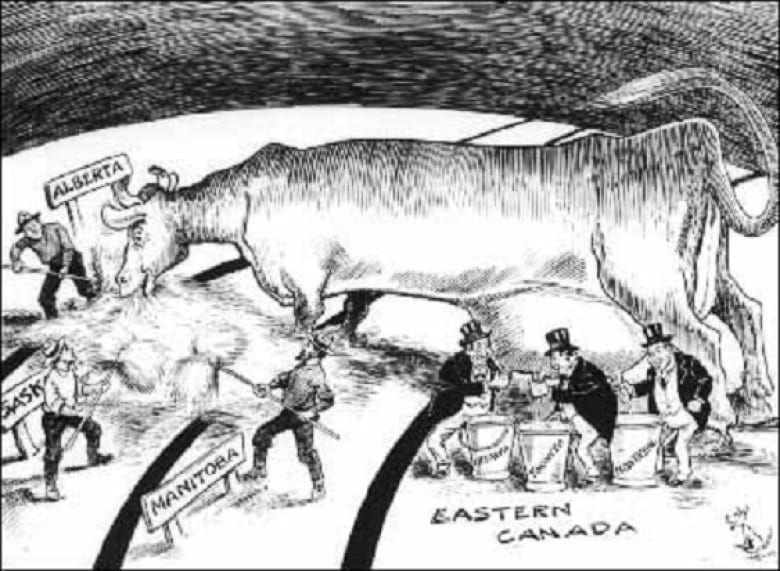

Unity across Canadian provinces is tenuous at the best of times; the current federation will likely fracture in a matter of decades. The distribution of resources, cultural differences, and geographical vastness will inevitably prove untenable. At the crux of the tensions between various provincial governments and their federal counterpart are an electoral system that is extremely seat heavy in the East, and an “Equalization Payment” system that systematically redistributes wealth from the “have” to the “have-not” provinces. Alberta is the archetypical “have” province, and sends billions of dollars annually to less productive provinces. Albertan independence is making its way back into the spotlight to some degree, but so long as it is under the Canadian financial umbrella, it is hard to take these rumblings seriously. There does appear to be a window of opportunity open with regards to a pair of monetary systems- gold and bitcoin- that are emerging as an alternative to the status quo. This status quo is “fiat” currencies, which in layman’s terms means that they’re backed by nothing, and can be created on a whim.

An aside- a staple of the reading list in the bitcoin realm is a non-fiction book written in 1997 called “The Sovereign Individual”. In it, the authors use broad analysis across a wide range of subjects to paint a picture of the future as it is shaped by computers, the internet, and the bursting of sovereign debt bubbles. More than a couple of their forecasts have been validated as having been uncannily accurate. Among the prophecies of theirs which have been fulfilled is the rise of an anonymous digital cash (bitcoin), and insolvent governments using a pandemic as an excuse to suspend the mobility rights of their citizens to keep them paying taxes within national borders. It is somewhat noteworthy, then, to point out that they also predict Alberta’s departure from Canada.

Western alienation is nothing new in Canadian politics. Typically, calls for succession become louder and louder during periods in which Liberals hold federal power as they snub the overwhelmingly conservative West, increase taxes, appease the green fanatical crowd/assorted other radical leftist cliques, and so on and so forth. These calls for separation tend to quiet down once a Conservative government forms in Ottawa, as these parties tend to be at least not overtly contemptuous of the West. The Conservative Party of Canada has just elected a shiny new leader who says all the right things in Pierre Poilievre -he even says he’s pro bitcoin, too! At the same time, blackface aficionado Justin Trudeau’s incumbent scandal ridden Liberal party is looking increasingly tired and incompetent. Given the shift in momentum politically, one might think that we are simply entering the next period of ebb and flow for interest in Western Canadian separation, and that the cycle described above will simply continue to repeat itself. There are a number of compelling reasons to believe, however, that things are different this time.

High, sticky inflation, unsustainable debt to GDP, decades of underinvestment in western fossil fuels in favor of inadequate renewables, Putin’s invasion of Ukraine (and the western response), supply chain disruption, and the COVID fallout- all are phenomena from within the last couple of years whose eventual resolution cannot possibly make all parties involved happy. Beneath all of this turmoil too are rapidly compounding deflationary pressures brought about by technological gains; kryptonite to a financial system that demands growth. Alberta, as an energy producing jurisdiction that runs perpetual surpluses (until of course, the feds take their cut), stands to be a loser not for its own shortcomings, but because of the fact that its fate is tied to that of the Canadian Federal Government.

“Since 1991, all 18 other governments with deficits exceeding 11% of GDP and debt to GDP ratios exceeding 110% defaulted within two years.”

-Hirschman Capital, January 2022 (in reference to the US approaching this threshold)

*Note: Defaulting on debt in this case does not just mean failing to make payments. Countries that have their own currencies historically avoid defaulting in nominal terms by printing the money to cover their debt- debasing their currency in the process. This is known as a soft default- on paper the debt is repaid but in “real” terms it is not, as the value has been inflated away

Canada’s debt to GDP in 2020 was 117% and its deficit was 11.36%. Now, that may have been an exceptional circumstance due to the COVID response, but the writing is on the wall. Canada’s national debt is $1.2 trillion dollars CAD (about $890 billion USD) Today, debt to GDP has fallen a bit for Canada, but it is still well over 100% and by many estimates is near the 110% mark noted above. Furthermore, it should be noted that GDP is a relatively easy metric to manipulate (just ask the CCP about the growth targets China hits without fail). Simultaneous to this very high debt to GDP level are a slew of recessionary factors. The Bank of Canada is pursuing a mandate of jumbo (0.75%-1%) rate hikes. Real estate accounts for 6% of Canada’s GDP -that’s a disproportionately large number and makes the economy very sensitive to these aggressive raises in interest rates. Unemployment is rising, and 3/4 of those jobs that did get added recently are in the public sector- meaning they add to inflationary government spending (Sorry Chrystia Freeland- a bunch of new government jobs is not a sign of a vibrant economy). Food inflation is double digits by any honest measure (aka not the official CPI rate) and in predictably anti-logical fashion the federal government’s response is billions in inflationary handouts.

Contrasting Canada’s economic outlook is Alberta’s current and historic economic performance; the differences are stark. Alberta is forecasting a 13 billion dollar surplus this year, much of it going towards paying down its own debt- which burdens the province ONLY because of equalization payments, and Canadian Health/Social transfers to other provinces. Alberta’s debt is somewhere around the $100 billion mark, the bulk of which was added in the past decade by the socialist NDP party (no surprise there), who gained power for a single term when conservatives split the vote in 2015. Even by conservative estimates Alberta would currently have a large surplus and no debt, had it not been for the money it sent to the federal government and other provinces. Most of the figures I could find put Alberta’s net outflows of cash to the rest of Canada in the $600 billion range over the last half century or so.

Equalization payments in particular are a flagrant assault on the prosperity of the West, and add insult to injury. Canada’s inability to supply their supposed allies in Europe with the cheap energy those nations need to counter the Russian supply taken offline this year is thanks solely to Eastern Canadian opposition to pipelines. Most ironic is the contempt for Alberta demonstrated by French speaking Quebec. In order to make it to the European market, Albertan resources would need pipelines to cross through Quebec, whose Premier in 2018 dismissed Albertan energy as “dirty” and “socially unacceptable”. Apparently the royalties from Albertan oil and gas are plenty acceptable in Quebec, as the province received $13 billion in equalization payments the year that comment was made, a similar figure this year, and billions more every other year for the better part of a century without fail.

Let’s put things in perspective here: Norway, with its sovereign wealth fund of $1.3 trillion USD, raised via oil and gas revenues, can be used as a striking analogy for the absurdity of this arrangement. Imagine if, instead of having the healthy balance sheet it does, Norway was forced to send its wealth to less well off states in the EU. Then, imagine that Quebec, which is about as far from Alberta as it is from Norway, somehow prevented Norway from supplying Europe with energy during an energy crisis resulting from a trade war with Russia. Now at the same time, imagine Quebec accepting a share of the profits from the energy Norway did manage to get to the market. This is exactly what is happening in Canada. Furthermore, the equalization payments system creates a perverse incentive structure; by providing a free and lucrative revenue stream, parties like Quebec and certain voters in the Maritime provinces have reason to reject economic development at home, as it would mean similar income for much more work. The same dynamic applies to a degree in Alberta, but in reverse; why develop more if it will just mean a bigger Federal hit each year?

On a side note, LNG export facilities on Canada’s East coast would also allow our natural gas to displace coal in developing nations like India. This displacement of coal use is perhaps the single most impactful thing that could be done to reduce emissions worldwide. Unfortunately, it is not palatable to Greta Thunberg and her grown-up cheerleaders in government, so these markets continue to burn coal, and buy their energy largely from- who else- Vladimir Putin.

Canadian policy makers pondering energy

Had there been means of exporting Albertan energy on Canada’s East coast, the situation unfolding in Europe right now would undoubtedly look very different. Whether or not Ukraine would have been invaded at all had Europe not been so dependent on cheap Russian gas and other commodities is entirely debatable. European countries now facing in some cases >1000x% increases in power costs are stocking up on firewood, and are scrambling to find people in retirement homes who know how to run old coal fired power plants in order to survive the winter. Russia, despite being cancelled by the west via sanctions, has seen an increase in their energy revenue, simply by selling a higher volume at a discounted price to trading partners like China and India. In what is as much a trade war as it is a kinetic war, G7 nations are engaged in nonsense like setting a price cap on Russian oil (a commodity they do not control), rather than flooding the market to crash prices. The latter is something they couldn’t do even if they wanted to, as such production is a time consuming, capital intensive process that has been neglected for a couple of decades in favor of vastly inferior unreliable renewable energy infrastructure. The skilled labor needed to bring these resources online for the West is increasingly non existent as well, due to workers retiring or switching industries.

In a stunning public denial of reality less than a month ago, Justin Trudeau expressed skepticism that there is a “business case” for LNG exports to Europe, despite German Chancellor Olaf Scholtz explicitly saying there is (as if it isn’t obvious). For decades, Alberta has been villainized domestically for producing fossil fuels- despite being one of the most ethical producers in the world. Idealism, an unfortunate byproduct of the peace and prosperity Canada has enjoyed in recent decades, has give rise to a utopian environmentalist movement that has gained considerable political leverage in Ottawa. Denying of the laws of physics and economics, the policy aspirations of this movement make it indistinguishable from a doomsday cult. Despite the claims of ESG proponents, it simply isn’t possible to transition advanced economies to less dense energy sources without significant fallout. Energy is a ubiquitous economic input, so “fallout” in this case means consequences like food shortages and outright economic failure. The utter collapse of Sri Lanka that happened just months ago is a direct result of ESG policy. Policy, it should be noted, that the Trudeau government now seeks to emulate here. Europe will soon be feeling the full brunt of this ideological commitment; winter is coming. Below is a photo of Steven Guilbeault, Canada’s “Minister of Environment and Climate Change” being arrested for an activism stunt. In case you missed it, the G7 nations are currently engaged in a hybrid war against Russia and various other anti-western states- a conflict which some observers have asserted is actually World War 3. Energy supply is literally one of the battlefields. Having an ideologue like Guilbeault anywhere near the levers of power regarding energy policy is absolutely unacceptable from a national security standpoint- but it is reality for Albertans in their union with Canada.

Climate czar and overall level-headed dude Steven Guilbeault

There is no shortage of examples of Alberta being handicapped by the rest of Canada. Calling the examples listed thus far “self defeating” would be polite, to say the least. The energy and financial crises we are facing are in their early stages. As they unfold there is bound to be an inflection point in popular sentiment towards independence amongst Albertans. What was a tolerable but very annoying arrangement can very easily turn into something much more dire, and fast.

“From the Bretton Woods era backed by gold bullion, to Bretton Woods II backed by inside money (Treasuries with un-hedgeable confiscation risks), to Bretton Woods III backed by outside money (gold bullion and other commodities)… After this war is over, “money” will never be the same again…and Bitcoin (if it still exists then) will probably benefit from all this.”

-Zoltan Poszar, “Bretton Woods III", March 7 2022

Written days after the start of the Ukraine invasion earlier this year, Credit Suisse gigabrain Zoltan Poszar’s predictions have proven to be on point thus far. This is good news for commodity rich, energy exporting Alberta, IF it can diverge from Canada, who stands to lose bigly in the coming new monetary order like the rest of the G7 nations. Nobody will ever really know Vladimir Putin’s true motives for invading Ukraine, but it seems increasingly likely that getting out from under the US Petrodollar system was a big factor. In his own words in August 2022; ''The economy of imaginary wealth is being inevitably replaced by the economy of real and hard assets”. Echoing Polszar from earlier in the year, its’ obvious that Russia knew sanctions were coming, and called BS on the credit addicted economies of the G7. So far, it’s worked, and all other currencies have weakened against the rouble since then . It’s hard to picture Canada in a position of strength any time soon given this set of circumstances. The Bank of Canada can and will print more dollars (Loonies as we call them here), but energy cannot be printed. How to store the value created from the sale of energy is the million billion trillion dollar question facing all energy producers. One certainly doesn’t have to be a seasoned market analyst to be able to tell that Loonies ain’t it.

* GRC= Global Reserve Currency

There is mounting evidence that gold is reemerging as a settlement mechanism for international trade, particularly in energy markets. Gold bugs have been saying things along these lines for a long time, but Russia (world’s biggest energy exporter) being kicked out of the SWIFT payments system is a catalyst for change that wasn’t present before. The BRICS (Brazil, Russia, India, China, South Africa) coalition- combined population of 3.22 billion- have signaled that they are on board with the creation of a commodity backed currency to rival US hegemony. “Commodity backed” may be misleading- use of most commodities as collateral is likely to cause unnecessary price inflation in said commodities by restricting supply in the face of industrial demand. Gold, with its’ relatively limited industrial use among other characteristics that make it suitable for use as money, is implicitly going to be the commodity used. China and Russia have both been selling US bonds and buying gold for years, lending credence to the idea that this schism with the existing financial system was premeditated; the sanctions against Russia included in these calculations.

Settlement of Russian energy contracts in gold is likely already happening. As mentioned earlier, Russia is compensating for sales lost due to sanctions by selling its energy to eastern trading partners at a discount. Chief among these partners are China and India (who incidentally launched an initiative to push back on price manipulation of gold bullion this year). The rate at which physical gold is being withdrawn from the COMEX (a preeminent precious metals exchange) is unprecedented. Buying physical gold from western markets and selling it at a premium to Russia in exchange for oil would be exactly the same as buying oil at a discounted price. This maneuver would allow Russia to accumulate more gold and gradually reprice gold in oil. The oil market is many, many times bigger than the gold market; doing so would lead to gold rapidly appreciating in value several orders of magnitude higher. By doing this, China and Russia could gradually drain gold from the West, and the latter could also offset the loss of the its seized FX reserves (roughly 20% the Russian Central Bank’s reserves are in the form of gold) Whether or not this is actually the case, big money is definitely removing gold from exchanges.

The “Gold to Oil Ratio” (price of a barrel of oil denominated in gold) has remained relatively steady historically. Due to inflation, confiscation, sanctions, and general geopolitical uncertainty, sovereign debt and fiat currencies are no longer a suitable store of wealth for oil profits even in the short term. Alberta following the BRICS nations’ lead by allowing gold to play a role in its energy markets would not be an act of allegiance to them, it would be acknowledgment of an economic reality. Accumulating physical gold reserves and settling commodity contracts in physical gold should both be in consideration for Alberta, although appetite for the latter is unlikely until the fiat system has deteriorated further.

As gold reenters the global monetary system, collective consciousness will undergo a paradigm shift with regards to what is valuable, and what makes it so.

Enter Bitcoin.

In essence, the largest surplus countries’ fiat currencies will implicitly grow their gold or commodity backing. Over time, these countries like China will have the “hardest” fiat currencies due to the asset composition of their reserves. Deficit countries globally, but particularly in the West, will have the weakest currencies as gold and commodities flow from West to East.

The price of gold will phase shift multiples higher than it is today. Trade happens at the margin, and faced with an indiscriminate buyer (all countries that earn fiat money internationally), it will inexorably march higher. This is a medium to long-term play (over the next decade); in the short-term, expect slow, creeping appreciation coupled with bouts of extreme downside volatility…

…Bitcoin is currently tied at the hip with big tech risk assets. If we believe nominal rates will go higher and cause an equities bear market and an economic recession, Bitcoin will follow big tech into the latrine. The only way to break this correlation is a narrative shift on what makes Bitcoin valuable. A rip roaring bull market in gold in the face of rising nominal rates and global stagflation will break this relationship.

As gold marches its way above $10,000, Bitcoin will march its way to $1,000,000. The bear market in fiat currencies will trigger the largest wealth transfer the world has ever seen.

-Arthur Hayes, “Energy Cancelled” , March 16 2022

Every 100 years or so, the global reserve currency changes. We are currently moving from a unipolar world of America and USD to a multipolar world of neutral reserve assets. China and Russia might be cooperating to undermine American influence, but they certainly do not trust each other. Thus, neutrality will be of the utmost importance in how sovereigns store their wealth and trade with one another going forward. Gold and bitcoin are the only two currencies that meet the criteria of neutrality. Bitcoin is objectively better than gold, and although gold may be the instrument that unseats the dollar, it is highly likely that Bitcoin outperforms it over time. For those readers who are still unfamiliar with the value proposition of bitcoin, I will again refer you to the essay I referenced at the beginning of this article

Proof of work mining and its energy consumption make bitcoin and Alberta a perfect union. Bitcoin mining is extremely competitive and energy intensive. Thus, mining bitcoin profitably while paying market rate is all but impossible, save for during black swan events like the Chinese mining ban and subsequent exodus of 2021. Not all power that is generated can make it to market due to a variety of constraints; this so called “stranded energy” is the ideal power source for bitcoin mining. An example of stranded energy would be power generated by wind turbines that is above and beyond market demand. In a situation like this with no conventional demand and no way to store it, without a “buyer of last resort” (bitcoin miners), it just gets wasted Alberta is Canada’s largest producer of natural gas; a process which creates a lot of stranded energy. Unused natural gas can be converted into electricity on site and used to earn bitcoin via mining. The possibility of connecting to the network via satellite makes even very remote sites eligible mining locations. Since this is gas which would not have made it to market in any case, the risk/reward dynamic of mining in these circumstances should be very enticing for energy producers. This should be an absolute no brainer for any energy company sitting on stranded energy, and could be an enticing way for the province itself to build up a reserve. Mined coins are easier to hodl and use discretely, which is ideal for what is bound to be an increasingly adversarial environment as things unfold.

If Alberta’s policy makers are sincere about defending property rights, granting bitcoin legal tender status within Alberta is an obvious step. This should be done while simultaneously rejecting KYC and AML laws (“know your customer”, “anti money laundering” respectively.) which serve the purpose not of protecting the public, but of state surveillance of private citizens. As we saw in February with the truckers’ protests, your money isn’t really yours if it’s held in a commercial bank. Should you so much as donate to a cause that is in opposition to the current regime, your ability to transact can be censored. This can not be allowed to happen again. The current frontrunner in the race to become Alberta’s next Premier, Danielle Smith, has a piece of proposed legislation called the “Alberta Sovereignty Act” at the center of her platform. Judging from her apparent success, Albertans do currently have an appetite for independence. However, when push comes to shove, being wholly within the domain of the Canadian financial system will give Ottawa the power to neuter any real pushback with relative ease. Should tensions rise with the federal government, another bank account freeze would be an obvious non-violent measure taken against dissidents. After all, the feds have a taste for this kind of thing now. Furthermore, in the mathematically assured event that the Canadian dollar collapses in value (don’t say it…don’t say it…don’t say it…hyperinflation!), having an alternative in place will spare Albertans from having to barter, participate in civil unrest, and engage in the rest of the activities that are necessitated by currency failures.

The price of energy is rising by double digits percentages, and that’s a modest estimate. Depending on where you live, this inflation could be measured in triple or even quadruple digits. On the other hand, the Canadian dollar is devaluing by double digits annually. Energy inflation will not slow down for a very long time, and the Loonie will lose value in perpetuity. There is no logical reason for any individual or business that makes their living in energy or any other genuinely productive activity to participate in a financial system designed to strip value from everyone who takes part in it, to the benefit only of the Government and their proxies. The demand for Albertan resources WILL outlive the Canadian dollar. Transitioning away from fossil fuels will be a decades long process and even then they will be needed as a reliable backup to nuclear (Sorry climate cultists- at least bitcoin mining can make all those ugly wind turbines taking up Southern Alberta agricultural land a little more economically viable though). Given the reality of this circumstance, it is obvious that at some point, a transition to a different financial system will need to be undertaken. The loss of confidence in central banks and the rise of a multipolar world make it clear that hard money will be demanded. The earlier that market participants acknowledge this reality, the greater they will be rewarded for being a first mover. Gold will lead the way, and Bitcoin will almost certainly supplant it. For a province with an embarrassment of riches, both human and resource wise, a hard money standard will be a most welcome change.

BARS

Great read, big up !